Pfizer: Rejuvenated Innovation Engine at a Discount

Summary

· Pfizer shares have fallen over ~50% since their COVID-19 era peak in December 2021.

· Company is much more productive and innovative today compared to its past, boding well for the future of its pipeline.

· Management predicts LOE revenue contraction to be offset by diverse new product launches and M&A, providing growth through 2030 and beyond.

· I view shares as undervalued below $30.

Hard Times for a Historic Company

In 2020, the COVID-19 pandemic sent viral shockwaves throughout the world, leaving a gloomy trail of death and destruction in its wake. Scientists worked around the clock to discover a safe and effective vaccine capable of halting disease sequalae and thus allow humans to resume normal life. The most successful of these efforts was brought to fruition by Pfizer in partnership with the small German company BioNTech, whose mRNA-based vaccine Comirnaty raked in global sales of $36.8B and $37.8B in 2021 and 2022, respectively. However, as COVID-19 gradually transitioned from pandemic into an endemic illness, Pfizer was left vulnerable to a dramatic contraction in vaccine revenues. Indeed, in 2023 Comirnaty sales sharply declined to $11.2B, and management forecasts 2024 top-line will be approximately $4B as annual COVID-19 boosters elovle into a seasonal product. A similar trajectory was observed for their COVID-19 antiviral product Paxlovid, further exaggerating revenue declines. Adding insult to injury, numerous best-selling portfolio medicines are expected to lose patent protection in the coming years, bringing into question future revenue growth in the face of a COVID-19 sales “hangover.” Wall Street has not reacted positively to these developments, with the stock declining over 50% from its all-time high of ~$59 per share in December 2021 to a recent low of ~$25 in April 2024. I believe the generally negative sentiment weighing on shares is overly pessimistic considering numerous encouraging assets poised to deliver sustainable growth of the company through 2030 and onward despite fears of patent expiries and generic competition.

Figure 1. Pfizer stock price over trailing 5-years. Source: Yahoo Finance.

A Renewed Focus on Discovery

Underpinning my optimistic long-term view of the business is a dramatic improvement of Pfizer’s R&D prowess over the past decade. Bringing new drugs to market is a fundamental driver of success in the pharmaceutical industry and, as such, is a critical metric to evaluate. In my opinion, the historic rate of positive R&D execution reflects the quality of management teams within a company and their collective judgement regarding capital allocation. There will always be failures within a discovery pipeline, but accurately identifying and focusing on assets with an above average probability of success is as much an art as it is science and, considering the intensive cash demands of modern drug development, has serious financial ramifications. Moreover, proficiently appraising internal pharmaceutical candidates is vital for building quality financial models, as net-present value (NPV) estimates are strongly influenced by expectations surrounding clinical trial performance, likelihood of FDA approval, and market uptake [1]. This calculus is largely the same for M&A considerations, thus impacting acquisition valuations and eventual realized rates of return. In essence, I like to view historical R&D success as an important (yet imperfect) metric for evaluating the reliability of financial expectations by management, since long-term projections inherently depend on assumptions related to clinical developments within the pipeline. This holds true for both new products, as well as growing existing products into new indications.

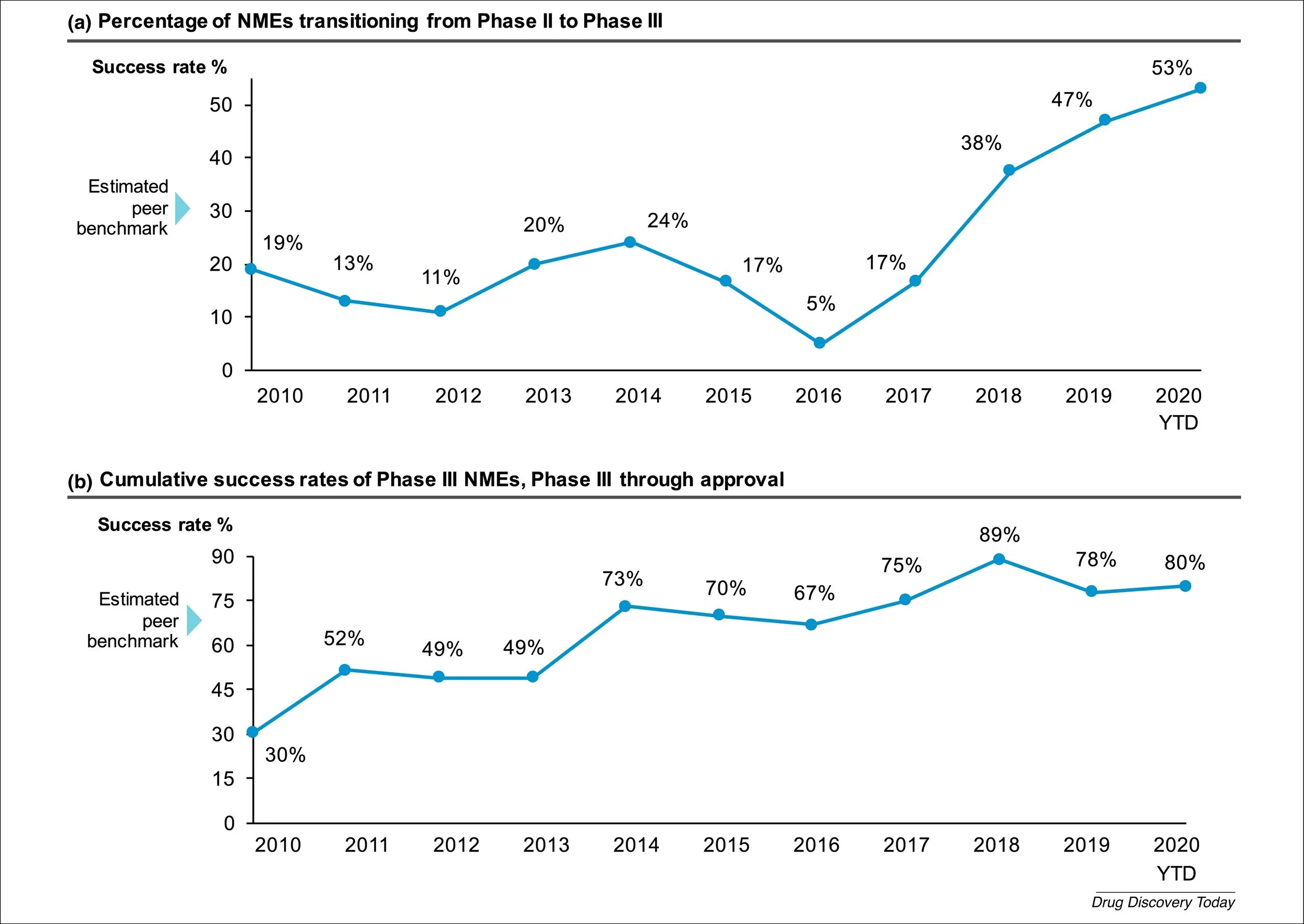

Figure 2. Pfizer Phase II & III Success Rates, 2010-2019. Source: Figure 1 from Wu, S.S., et al., Reviving an R&D pipeline: a step change in the Phase II success rate. Drug Discov Today, 2021. 26(2): p. 308-314.

To those who have not closely analyzed Pfizer in recent years, the 175-year-old company is not likely a name that immediately comes to mind when thinking of pioneering and forward-thinking organizations. However, the company’s revenue composition has profoundly shifted in the past decade as it divested virtually all business units outside of its innovative, patent-protected drug discovery and commercialization segment. The result has been a modernized, streamlined Pfizer focused squarely on bringing novel medicines to patients – no more operations in business areas like generic drugs, animal health, consumer health, and nutrition. Similar divestures have been the trend among large pharmaceutical companies as margins and revenues in these segments have eroded from increasing competition by low-cost producers and changing consumer spending behaviors. Many are enticed to pursue novel drug discovery considering its very attractive margins and barriers to entry formed by patent protection, market exclusivity, and regulatory requirements. However, exceedingly high failure rates make this business model financially intensive and requires that a small number of very profitable medicines offset the many losers. Moreover, companies must perpetually invent or acquire new products to counterbalance revenue decline from competing generic medicines once a drug loses patent protection. Thus, the ability to consistently discover, develop, and commercialize novel drugs is paramount for ensuring long-term prosperity in the pharmaceutical business.

To combat these unending challenges, Pfizer has worked to drastically improve their R&D productivity over the last decade. In the early 2010s, the company substantially lagged peers in terms of success rates for advancing new-molecular entities (NMEs) through clinical trials and approval into the marketplace [2]. Pfizer therefore performed a retrospective analysis in 2012 of phase II success rates among 44 NMEs between 2005-2009 to better understand the causes of program failure and termination [3]. Based on these initial findings, management has embarked on a multiyear turnaround campaign to continuously improve the quality of their R&D organization. Efforts have largely focused on prioritizing science, deeply understanding disease biology, and narrowing the range of therapeutic areas (TAs) under investigation from ten to five.

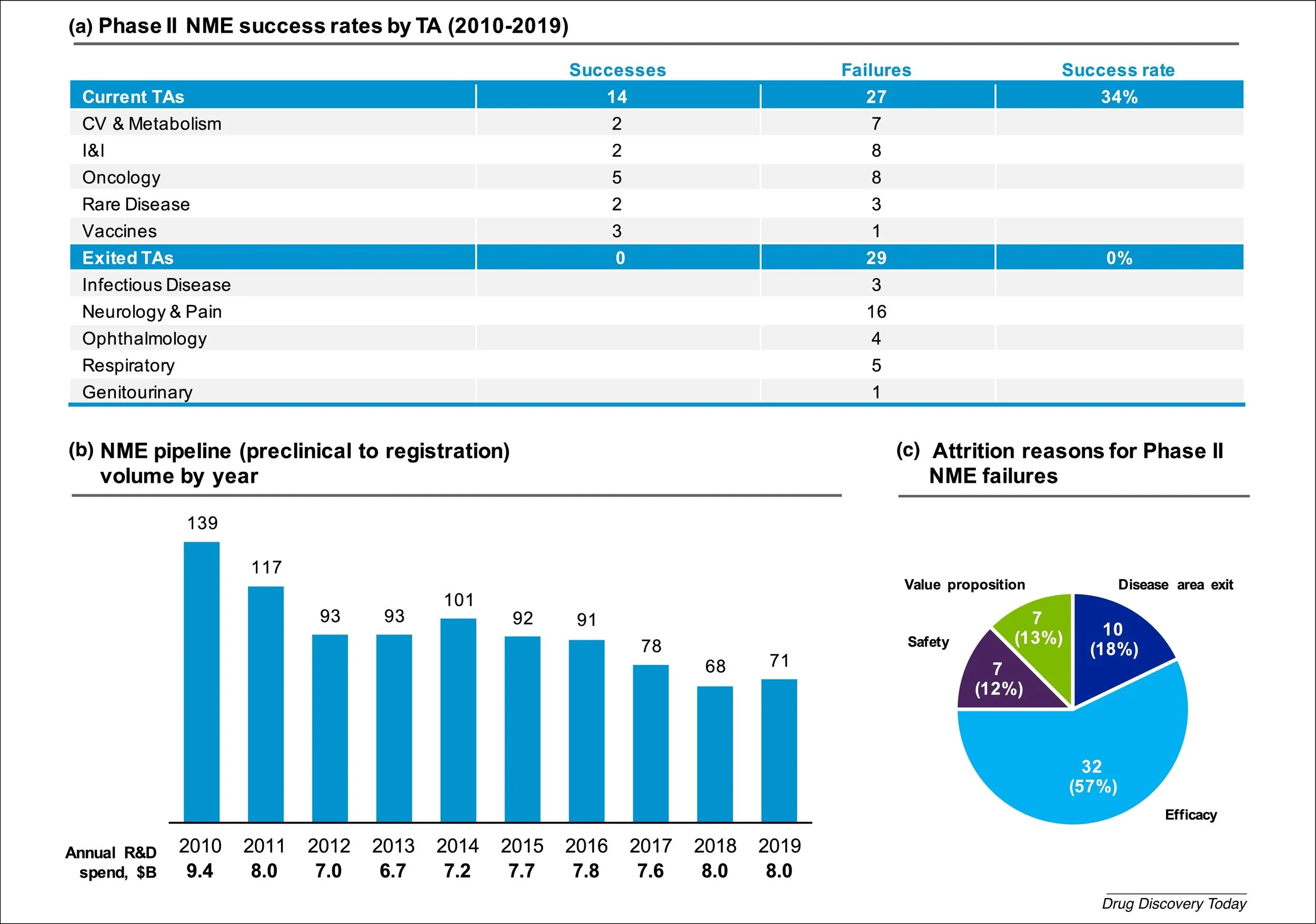

Figure 3. Pfizer Phase II Success Rates by Treatment Area. Source: Figure 2 from Wu, S.S., et al., Reviving an R&D pipeline: a step change in the Phase II success rate. Drug Discov Today, 2021. 26(2): p. 308-314.

The company determined that among the various TAs, there were stark differences in the rate of program failure. In fact, between 2010 and 2019, five out of the ten TAs being explored had a 100% failure rate [2]. These underperforming segments clearly had an outsized impact on overall portfolio success and were subsequently exited entirely. This strategy of limiting TA breadth aims to concentrate resources into areas where disease biology is better understood and thus provide a better opportunity for positive outcomes. Today, the pipeline is focused in the areas of oncology, inflammation and immunology, vaccines, internal medicine, and anti-infectives. Commensurate with narrowing their TA focus, the number of programs in clinical development has slowly decreased over time, from 139 in 2010 to 71 in 2019 [2]. Importantly, the annual R&D spend over this timeframe has remained fairly even, meaning the budget per program has increased substantially. As a scientist, this logic makes inherent sense to me – the success of a laboratory project can often be strongly influenced by the amount of resources dedicated to it. In other words, making sure there is an adequately large budget and team of scientists on any given project is critical for ensuring that research efforts result in definitive information that can be used to make go/no go decisions for extending or terminating an R&D campaign.

In addition to limiting TA scope, Pfizer has worked on expanding the variety of drug modalities within their toolkit. Historically, and still today, the company has exceptional capabilities in medicinal chemistry and small molecule drug development. While small molecules are very effective against many protein targets, the majority of the proteome cannot be adequately drugged with traditional inhibitors [4]. Accordingly, a slew of biotechnologies that enable targeting more challenging proteins or complex diseases have been developed over the years such as antibodies, siRNAs, mRNA, antibody-drug conjugates, targeted protein-degraders, and gene therapy. Over the 2010-2019 timeframe, Pfizer has substantially lessened its dependence on small molecules by increasing the percentage of biologics and other innovative modalities in its pipeline [2]. Today, the company has access to a wide range of biotechnologies that were either developed internally, acquired via M&A, or licensed through partnerships.

Figure 4. Pfizer New Pipeline Modalities. Source: HRG and adapted from Figure 3 Wu, S.S., et al., Reviving an R&D pipeline: a step change in the Phase II success rate. Drug Discov Today, 2021. 26(2): p. 308-314.

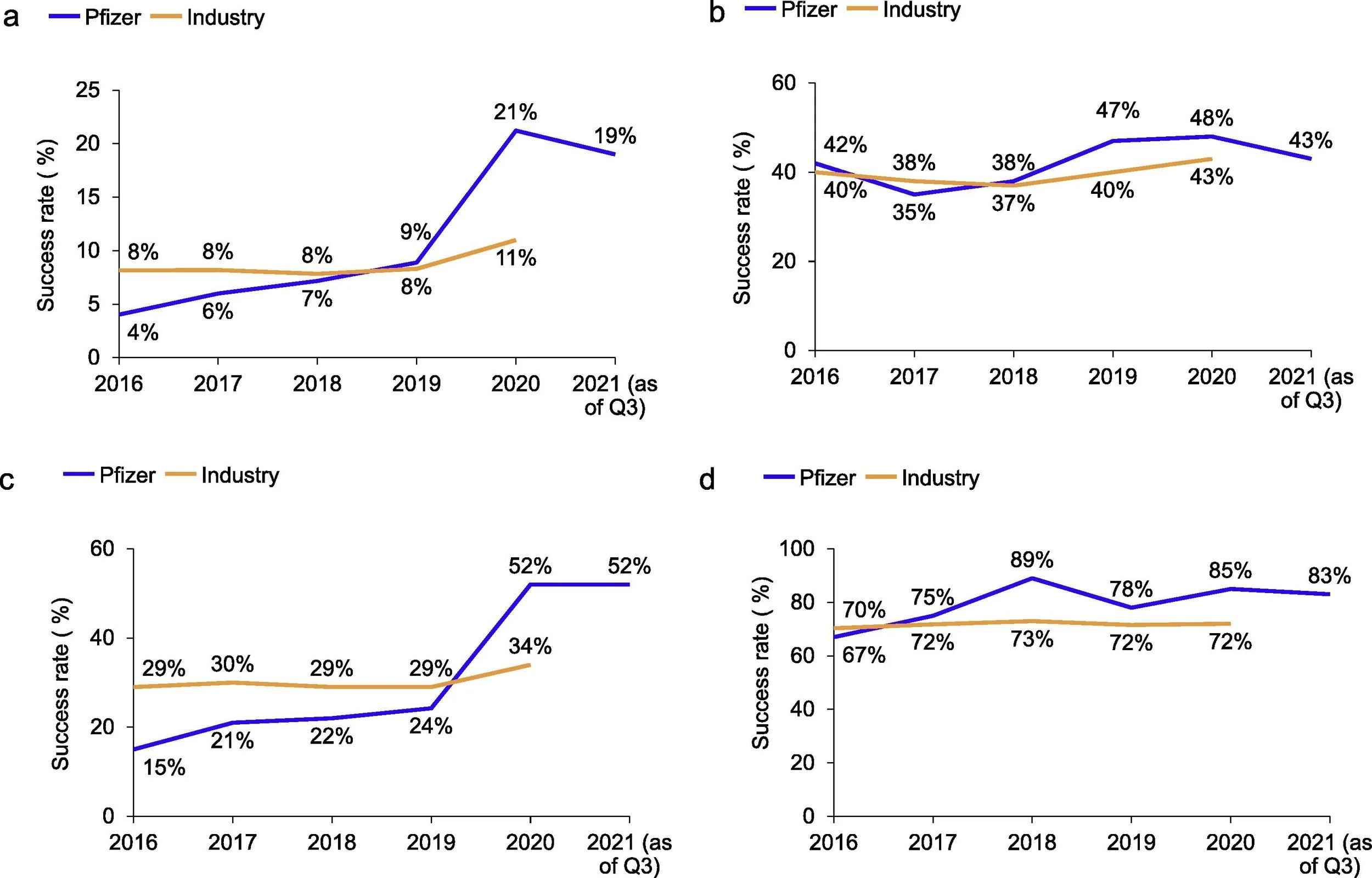

These years of focus on science and execution appear to have paid off. The overall pipeline success rate, as measured by cumulative first in human (FIH) studies to FDA approval, has drastically improved over time [5]. In 2020, Pfizer boasted a 21% FIH to approval success rate, almost 2x the industry average of 11%. This is a remarkable ~10x increase from their meager 2% success rate in 2010 (industry average 5%). Underscoring the nimbleness and productivity of the revitalized Pfizer R&D is the creation of both a vaccine and antiviral medication during the COVID-19 pandemic. These drugs were developed with unprecedented speed and subsequently commercialized on a global scale without historical parallel, demonstrating the efficiency and effectiveness by which this business now operates. Importantly, their COVID-19 success does not appear to have resulted from accidental good fortune, as the Pfizer FIH to approval rate was steading increasing prior to COVID-19, rising ~2x from 4% in 2016 to 9% in 2019. While the future is never absolutely certain, forward-looking prospects for the business look encouraging. Wall Street seems to currently have mixed feelings towards Pfizer, but management has presented a more optimistic view of operations through 2030 and beyond. Considering the notable R&D turnaround, a string of intelligent acquisitions, and recent product approvals, I am inclined to share management’s positive outlook over the long-term.

Figure 5. Clinical Success Rates vs Industry, 2016-2021. Rates are shown as a rolling average over 3 or 5-years. A) Cumulative FIH to approval. B) Phase I to phase II transition. C) Phase II to phase III transition. D) Phase III to approval. Source: Figure 1 from Fernando, K., et al., Achieving end-to-end success in the clinic: Pfizer's learnings on R&D productivity. Drug Discov Today, 2022. 27(3): p. 697-704.

Growing Through the Turmoil

Analyst reports over the past 12 months have largely expressed a neutral or bearish sentiment, citing anticipated patent expiries that will weigh on revenue growth in the 2025-2030 period. Flagship products Eliquis, Ibrance, Vyndaqel, Xeljanz, Xtandi, and Inlyta made up a combined ~$18B of total revenue in 2022 and are all facing loss of exclusivity (LOE) in the 2024-2027 period. As a result, it is predicted that sales for these key products will steadily erode to ~$1B by 2030. While this may seem alarming at first glance, the company has a deep portfolio of newly launched medicines that management expects to counterbalance revenue deterioration from LOEs through the end of the decade. Crucially, sales from newly launched non-COVID products are expected to reach ~$20B on a risk-adjusted basis by 2030, more than offsetting any impact from LOEs over this timeframe. At the time of writing, Pfizer is in the process of launching 19 new products or indications over an 18-month period. According to CEO Albert Bourla, this is the most vigorous product rollout in company history. These launches cover a diverse range of TAs and modalities, spanning areas such as oncology, immunology, or vaccines and use numerous approaches including small molecules, antibodies, mRNA, and more.

Figure 6. 2025-2030 Revenue Projections and LOEs. Source. Pfizer 2Q23 Earnings Presentation.

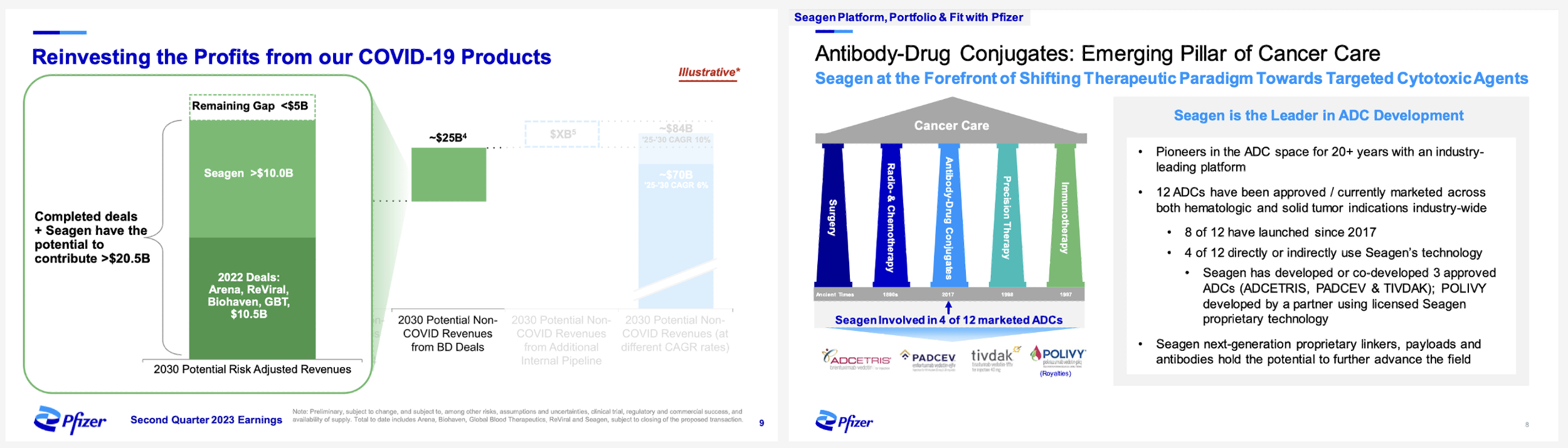

In addition to the new rollouts mentioned above, a string of M&A has further bolstered the Pfizer asset collection and is projected to deliver top-line growth from 2025-2030 and beyond. Together, sales of these acquired medicines are estimated to be ~$25B by 2030 on a risk-adjusted basis and form an important component of the bullish thesis. During the COVID-19 pandemic, mRNA vaccine Comirnaty and antiviral Paxlovid drove total company revenues to a historic $81B and $100B in 2021 and 2022, respectively. This unusually large bolus of cash strengthened the balance sheet at an opportune moment when Pfizer was (and still is) facing an imminent patent cliff. As a result, management reinvested these earnings over the last three years by acquiring seven companies for an approximate consideration of ~$70B in aggregate. The largest, and arguably most important, acquisition was that of Seagen for $43B in 2023. Seagen was a pioneer and leader in the space of antibody-drug conjugates (ADCs), a modality that is currently revolutionizing cancer therapy. You can read my thorough introduction to ADCs here. Buying the company allowed Pfizer to add four FDA approved medicines to its portfolio spanning several liquid and solid tumor types. Moreover, the acquisition included numerous pipeline assets with great potential and the very talented team of Seagen employees responsible for inventing and commercializing their approved products. Albert Bourla has emphasized to shareholders that this acquisition was as much for talent as it was for the ADCs themselves, an approach that is not very common in the industry.

Figure 7. Newly Launched Products and Recent Acquisitions. Source: HRG and Pfizer 2Q24 Earnings Presentation.

Pfizer has stated its intention to become a leader in oncology by applying learnings from Project Lightspeed, an internal set of operating principles conceived during the COVID-19 pandemic that allowed them to quickly focus resources to solve seemingly intractable therapeutic problems. As such, the company reorganized to create a specific Pfizer Oncology vertical that is managed separately from rest of its therapeutic portfolio. At the 2024 JPMorgan Healthcare Conference, Bourla said "The very important thing for Seagen was the way that we did the integration. Right now, 50% of people of the new Pfizer Oncology research group are coming from Pfizer. 50% of the people in the new Pfizer Oncology group come from Seagen. We have a leadership team that is driving the new Oncology business unit. 9 members are reporting to Chris Boshoff. 5 of the 9 are coming from Seagen, 4 are coming from Pfizer. We believe that because the integration was done in a way that we're able to inspire people from Seagen to join us in a common vision how to run the new Pfizer Oncology, that will deliver on the promise of becoming a world-class oncology leader." Considering the importance of ADCs for the future growth of Pfizer, I am very encouraged that such a large portion of Seagen employees have been retained to develop these assets into new medicines. Of the ~$25B in 2030 risk-adjusted revenues from M&A, approximately ~$10B is projected to come from Seagen and the remaining ~$15B from other acquisitions. These purchases offer nice complementarity by delivering exposure outside of oncology such as immunology and inflammation (Arena Pharmaceuticals), rare disease (Global Blood Therapeutics), and internal medicine/neurology (Biohaven), among others. Collectively, I see this assortment of new medicines as well positioned to deliver growth across a range of TAs and help to more than offset the impact of LOEs in the coming years.

Figure 8. Seagen Acquisition Rationale and Projected Revenue Impact. Source: Pfizer 2Q23 Earnings Presentation and Proposed Seagen Acquisition Slides.

The third pillar of growth for Pfizer, and the largest wildcard, are the pipeline assets with potential launches in the back half of the decade. Programs here cover potentially very large indications such as obesity (oral GLP1, danuglipron), lung cancer (B6A ADC), COVID/Flu combination mRNA vaccine, breast cancer (ER degrader, CDK4, CDK2), and many more. Although the success of these programs is uncertain and some are likely to fail, Pfizer’s greatly rejuvenated R&D capabilities instill confidence that a portion will readout favorably and provide upside to estimates that currently do not include these assets. Furthermore, there is also potential for additional M&A or licensing that is difficult to predict. Management has stated that over the near term (~12 months), their major priority is to de-leverage the balance sheet from the Seagen acquisition by paying down debt to a more reasonable level. However, they have stated their openness to more BD once the target debt level has been reached and hence future positive catalysts may emerge over the next 2-3 years. As this is impossible to anticipate with any precision, I view this as “gravy” to the upside and not at all necessary for the current bull thesis. Taken together, the suite of newly launched medicines, acquired assets, and future pipeline coalesce to form a persuasive narrative for sustained growth and, in my view, makes the business attractively positioned for the long-term.

Figure 8. Pipeline Medicines with Exciting Potential. Source: Pfizer 2Q24 Earnings Presentation.

Valuation

Pfizer stock has been under pressure for over two years, falling to a recent low of ~$25 in April 2024 from a high of ~$59 in December 2021 and marking a ~57% decline peak to trough. Shares currently trade around ~$29, resulting in a market capitalization of approximately $161B. Analysts predict 2025 EPS of roughly ~$2.59, giving a forward PE of ~11x that is projected to continually decline as earnings grow from 2026 onwards. I see an ~11x PE as relatively undemanding considering my optimism surrounding the future growth prospects of the business and stability provided by a diversified portfolio of medicines. I perceive there to be a sufficient margin of safety at the current share price given conservative projections of near and long-term financial performance. Management anticipates that approximately ~$17B of revenue will be lost due to LOEs by 2030, but this is more than offset by ~$45B+ of new drugs launching into the marketplace and future optionality from the pipeline. Even if these growth projections were wildly inaccurate and came in substantially less than ~$45B, I think one can conservatively assume that at a minimum, earnings will remain flat and thus provide an annualized earnings yield of ~9% (inverse of 11x PE). In a justifiably optimistic growth scenario, which I currently view as a base case, earnings will grow into 2030 and deliver earnings yields in excess of 10% annually. Qualitatively taking into account many factors such as 5 and 10-year treasury yields, competitive pressures, the Pfizer balance sheet, and overall market valuations, I see a potential ~10%+ annualized rate of return as quite attractive.

Figure 9. Pfizer Consensus EPS Estimates and Historical Dividends per Share. Source: Yahoo Finance.

A meaningful portion of total shareholder return is likely to come in the form of dividends which, at recent stock prices, is currently yielding ~5.9% annually. This stream of income provides downside protection to investors in the event of any market volatility and is expected to remain stable over time. Indeed, management has repeatedly stated their commitment to maintaining the dividend and are backed up by an 85-year track record of uninterrupted quarterly payouts. Furthermore, the per-share dividend has increased every year going back to 2010, boding well for future potential increases as earnings grow. Another method in which capital may be returned to shareholders is through share buybacks. While the buyback program has been temporarily suspended while they focus on de-leveraging the balance sheet, management has stated their open mindedness to resuming this in the future. Prior to the COVID-19 pandemic, the company was a routine buyer of shares during the 2014-2019 period, signaling their willingness to reduce share count with excess capital. Lastly, this analysis does not consider the possibility for a re-rating of the earnings multiple as confidence builds in the growth story. As interest rates are expected to fall in the coming months and clarity develops around new products and the pipeline, I would not be surprised if the PE expanded to be more in line with mega cap peers around 15x forward earnings. This of course would provide buoyancy to shares independent from actual changes in the business fundamentals.

Conclusions

While many investors are currently focused on the short-term uncertainties challenging Pfizer, I believe a more holistic consideration demonstrates that the future is bright for this historic business. Years of focused execution have revitalized their R&D capabilities to be on par or greater than the broader industry, and this sets them up favorably going forward. Cash from COVID-19 success came at a fortunate point in time and management capitalized on this by acquiring some highly attractive organizations and their assets. Based on conservative analyst estimates of forward earnings, I view shares as favorably priced under $30 with an adequate margin of safety in the event conditions deteriorate more than anticipated. There are always uncertainties in business, but Pfizer’s fundamentals have been consistently moving in the right direction over recent years from an invigorated commitment to science and discovery.

References

1. Stasior, J., B. Machinist, and M. Esposito. Valuing Pharmaceutical Assets: When to Use NPV vs rNPV. 2018 [cited 2024; Available from: https://www.alacrita.com/whitepapers/valuing-pharmaceutical-assets-when-to-use-npv-vs-rnpv.

2. Wu, S.S., et al., Reviving an R&D pipeline: a step change in the Phase II success rate. Drug Discov Today, 2021. 26(2): p. 308-314.

3. Morgan, P., et al., Can the flow of medicines be improved? Fundamental pharmacokinetic and pharmacological principles toward improving Phase II survival. Drug Discov Today, 2012. 17(9-10): p. 419-24.

4. Hopkins, A.L. and C.R. Groom, The druggable genome. Nat Rev Drug Discov, 2002. 1(9): p. 727-30.

5. Fernando, K., et al., Achieving end-to-end success in the clinic: Pfizer's learnings on R&D productivity. Drug Discov Today, 2022. 27(3): p. 697-704.

Author Disclosure Statement

I/we have a beneficial long position in the shares of PFE, BNTX, and ARVN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

HRG Disclosure Statement

Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of HRG as a whole. HRG is not a licensed securities dealer, broker or US investment adviser or investment bank. Authors are third parties that may include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.